Buy Property in Dubai on Installments: 2026 Buyer’s Guide

Quick answer: In 2026, you can buy property in Dubai on installments by paying a 5%–10% booking deposit to a developer, then settling the balance through scheduled milestone payments tied to construction. These developer plans bypass bank mortgages entirely, apply mostly to off-plan inventory, and sit under RERA escrow protection for buyer capital.

You no longer need millions in liquid cash to own property in Dubai. To buy property in Dubai on installments has become the default capital strategy for the 2026 cycle, replacing the old model of full upfront settlement with phased, developer-financed payment structures. This shift has opened the market to buyers who were previously locked out by loan-to-value ceilings and credit audits.

This guide covers installment buying across every asset class apartments, villas, townhouses, and commercial not a single narrow segment. It speaks to four distinct buyer profiles: first-time buyers without a large cash pot, budget-conscious investors chasing leverage, overseas non-residents phasing their capital streams across borders, and local expats sidestepping rising bank mortgage margins.

By the end, you will understand exactly how these plans work, every plan structure on the market, the strongest developers, the true total cost, the RERA safeguards protecting your money, the default consequences, and a full side-by-side comparison against mortgages and cash. If you want the broad market overview first, start with How to Buy Property in Dubai.

How Installment Plans Work in Dubai Real Estate

A developer installment plan is direct seller financing on off-plan inventory. The buyer reserves a unit, pays a booking deposit, then pays scheduled installments tied to verified construction milestones until handover. No bank sits in the middle.

The mechanics are straightforward. The booking amount is typically 5%–10% of the property value. From there, payments follow a developer payment schedule registered with the Dubai Land Department (DLD). Each installment is triggered by a construction stage foundation complete, structure topped out, MEP installed rather than an arbitrary calendar date.

This structure bypasses traditional bank credit audits. There is no mortgage pre-approval, no income verification against UAE lending criteria, and no LTV cap. That accessibility is precisely why developer-financed installments dominate among self-employed buyers and overseas non-residents who would face friction in the conventional mortgage channel.

One point demands absolute candor: installment plans apply almost exclusively to off-plan launch inventory, not ready-to-move-in assets. If you want immediate handover, you are looking at a cash purchase or a bank mortgage, not a developer payment plan. For the full transactional walkthrough, see Buying Property Process.

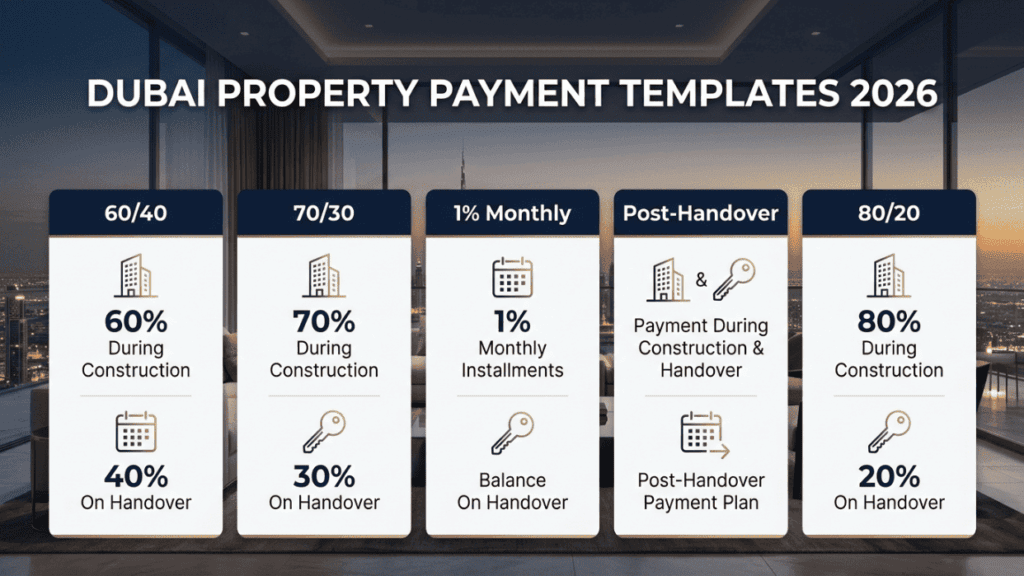

Types of Installment Plans Explained: Formats for Every Budget

When you buy property on installments in Dubai, the structure you select determines your cash velocity and your handover exposure. Five payment templates dominate the 2026 launch market, each calibrated to a different capital profile.

60/40 — 60% paid during construction, 40% at handover. The standard, most common plan across major developers.

70/30 — a heavier construction-phase commitment with a lighter handover balance. Suits buyers who prefer to clear more of the principal before keys.

1% Monthly — the most accessible structure on the market. Example: AED 10,000 per month on an AED 1M property. Built for budget buyers who prioritize predictable, low monthly outflow.

Post-Handover — installments continue after you receive your keys, often spanning two to five years past handover. Ideal for cash-flow-focused investors who want rental income to service the balance.

80/20 — a front-heavy build-phase payment with a minimal 20% handover amount.

| Plan Type | Booking | During Construction | At Handover | Post Handover | Best For |

| 60/40 | 5%–10% | 60% | 40% | — | Standard buyers wanting balanced exposure |

| 70/30 | 5%–10% | 70% | 30% | — | Buyers clearing principal pre-handover |

| 1% Monthly | 5%–10% | ~1%/month | Balance | — | Budget buyers needing low monthly outflow |

| Post-Handover | 5%–10% | 40%–60% | 20%–30% | 20%–40% | Cash-flow investors using rental income |

| 80/20 | 5%–10% | 80% | 20% | — | Buyers minimizing handover lump sum |

All Property Types You Can Buy on Installments

Installments are not confined to micro-apartments. Every major asset class in Dubai is available on developer payment plans, with pricing bandwidths that span entry-level to ultra-prime.

Apartments

Priced from AED 400K to AED 5M, apartments are available on installment plans through all major developers. This is the deepest inventory pool and the most accessible entry point for first-time buyers. See Buy on Installments for current listings.

Villas

Villas range from AED 2M to AED 10M and are offered on installments through Emaar, Nakheel, and Damac. Larger ticket sizes pair naturally with extended post-handover structures that ease the capital load. Explore Off-Plan Villas for the active pipeline.

Townhouses & Commercial Assets

Townhouses sit between AED 1.5M and AED 5M, available via Nakheel, Damac, and Emaar. Commercial units are offered on installments by select developers. Review [Buy Townhouse] for townhouse inventory.

Foreign ownership is fully permitted on installment purchases within designated freehold zones, and there is no residency requirement to buy. For eligibility and ownership rights, see Can Expats Buy Property and Freehold Property Dubai.

Best Developers Offering Installment Plans in 2026

The developer you choose shapes your terms as much as the unit you select. For buyers who want to buy property in Dubai on installments, the city’s foundational master developers each bring a distinct payment posture in the 2026 cycle.

Damac — the most aggressive installment plans in the market. The 1% monthly schedule is widely available across its portfolio, making it the entry point of choice for leverage-focused buyers.

Emaar — government-backed and reliable. The standard 60/40 structure across its launches is the benchmark for delivery confidence.

Nakheel — government-backed with competitive structured plans, strong on waterfront and master-community inventory.

Reportage Properties — the most affordable entry points, engineered for budget-conscious buyers seeking the lowest capital threshold.

Sobha — premium build quality with 60/40 plans and post-handover options on select projects.

Meraas — luxury 70/30 structures across its high-end, design-led developments.

Contact First Call Real Estate to compare the best installment plan properties across Dubai. → View installment listings

The True Cost of Buying Property on Installments

Headline payment splits tell only half the story. The complete cost picture includes statutory fees most buyers underestimate. Below is a worked example on a standard AED 1,500,000 villa under a 60/40 milestone structure.

- Booking amount — AED 75,000–150,000 (5%–10%)

- During-construction installments — AED 750,000 (50%)

- At handover — AED 600,000 (40%)

- DLD transfer fee — AED 60,000 (4%)

- Agent commission — AED 30,000 (2%)

- Total commitment — AED 1,590,000

The numbers reveal the strategic case for phasing. Rather than locking AED 1.5M into a single illiquid position, the installment buyer deploys a fraction upfront and keeps the remainder working.

The Capital Efficiency Formula: Utilizing an off-plan installment framework functions as a raw leverage multiplier. By deploying a minimal 5% to 10% initial booking deposit, an investor secures 100% of the underlying property’s market capital appreciation during the build phase while keeping the remaining cash reserve liquid.

This is the core difference between installments and a cash purchase. Installments eliminate cash drag, preserve liquidity for parallel positions, and maximize capital efficiency across a portfolio.

RERA Protection for Installment Buyers

Buyer capital on off-plan installment purchases sits behind multiple layers of UAE statutory protection. The framework is built to ensure your money funds construction, not developer overhead.

- All off-plan payments must be deposited into a RERA-regulated escrow account dedicated to that specific project.

- Funds are released to the developer only against verified construction milestones — never as a lump sum upfront.

- Independent civil engineering auditors verify build progress before each escrow release.

- Buyers have a contractual right to compensation if a developer delays beyond the terms of the Sales and Purchase Agreement (SPA).

- If a project is cancelled, a full refund from escrow is guaranteed.

- RERA Article 11 (the codified regulatory framework that governs developer termination timelines, grace periods, and asset refund brackets in the event of default) specifies refund entitlements when an SPA is terminated.

- DLD Oqood registration (the official Dubai Land Department system that registers your interim property title before physical construction handover occurs) proves your ownership interest from day one.

This is why buying property on installments in Dubai is safe when you transact through registered developers and DLD channels: the law ring-fences your capital, rather than relying on trust.

Speak to a First Call Real Estate specialist to find the safest installment opportunities in 2026. → Book a consultation

What Happens If You Cannot Pay: Navigating Default Risks

A missed installment does not trigger immediate forfeiture. UAE law mandates a structured cure process before any contract termination, and the rules favor an orderly resolution.

The developer must first issue a formal notice through the DLD, opening a grace period of typically 30 days. If the balance remains uncleared after that window, the developer may move to terminate the SPA. At that point, the buyer forfeits a portion of payments and critically, the forfeiture is on a sliding scale tied to the physical construction stage, not the full sum paid. RERA Article 11 governs these refund brackets and protects a defined portion of buyer capital.

⚠️ CONTRACTUAL DEFAULT AND GRACE PERIOD DISCLOSURE: Missing an installment milestone triggers strict legal processes outlined in your Sales and Purchase Agreement (SPA). Under permanent RERA rules, developers must issue a formal 30-day notice via the DLD. If the balance remains un-cleared, the contract can be legally terminated with sliding-scale capital forfeitures tied strictly to physical construction stages. Never halt scheduled milestone payments without a formal legal audit.

The single most important rule: never stop paying without a formal legal audit first. For a fuller breakdown of downside scenarios, read Risks of Buying.

Financial Breakdown: Installment Plan vs. Mortgage vs. Cash

Choosing a financing route is a capital efficiency decision, not simply a hunt for the lowest sticker cost. Each pathway carries a distinct profile across approval friction, interest exposure, and liquidity preservation.

| Factor | Installment Plan | Mortgage | Cash |

| Down Payment | 5%–10% booking | 20%–25% | 100% |

| Bank Approval | None required | Mandatory credit audit | None required |

| Interest | Zero | Variable bank rate | Zero |

| Property Type | Off-plan only | Ready or off-plan | Any |

| RERA Protection | Yes (escrow) | Partial | Yes |

| Capital Efficiency | Highest | Moderate | Lowest |

| Monthly Commitment | Milestone or 1%/month | Fixed amortization | None |

| Best For | Off-plan buyers maximizing leverage | Ready-property buyers needing financing | Buyers prioritizing zero ongoing cost |

The takeaway is clear. Developer installment plans deliver the highest capital efficiency of the three routes and require no bank approval, making them the most accessible path for off-plan buyers. A mortgage suits those buying ready property who need external financing. A cash purchase suits buyers who value zero ongoing commitment above liquidity. For phased, leverage-driven off-plan acquisition, installments win on every accessibility metric that matters.

Own Dubai Property on Your Terms in 2026

Installment plans have made Dubai property ownership accessible across every asset class apartments, villas, townhouses, and commercial with full RERA escrow protection standing behind every dirham. The model rewards the buyer who treats capital as a resource to deploy strategically rather than a sum to surrender in full.

Launch inventory absorption is accelerating through the 2026 cycle, and the strongest installment-plan units carry the fastest sell-through rates. The window to secure the best structures on prime stock is narrowing. The decision to buy property in Dubai on installments is, at its core, a decision to keep your capital working while your asset appreciates.

Contact First Call Real Estate today.

Frequently Asked Questions

How do installment plans work for property in Dubai?

You reserve an off-plan unit, pay a 5%–10% booking deposit, then pay scheduled installments tied to construction milestones until handover. The developer has registered the plan with the DLD, and no bank financing is involved.

What is the minimum down payment for property installments in Dubai?

The booking deposit is typically 5%–10% of the property value. On an AED 1M property, that means an entry capital outlay of AED 50,000 to AED 100,000.

Which developers offer the best installment plans in Dubai?

Damac leads on accessibility with widely available 1% monthly plans. Emaar and Nakheel offer government-backed 60/40 reliability, Reportage offers the lowest entry points, and Sobha and Meraas offer premium post-handover and 70/30 structures.

What happens if I miss an installment payment in Dubai?

The developer issues a formal 30-day DLD notice. If the parties fail to resolve the issue, either party may terminate the SPA, with forfeiture calculated on a sliding scale tied to the construction stage. RERA Article 11 protects a defined portion of your capital.

What is the difference between installment plan and mortgage in Dubai?

An installment plan is developer financing on off-plan property requiring no bank approval and charging zero interest. A mortgage is bank financing for ready or off-plan property requiring credit approval, a 20%–25% down payment, and interest payments.