How to Buy Property in Dubai | Pinnacle Investment

Knowing how to buy property in Dubai is a defensive, financially sound allocation of cross-border capital a move that places your wealth inside one of the few major markets engineered for tax-neutral returns. This guide speaks directly to cash buyers, self-employed overseas investors managing foreign funds, and resident expats upgrading their primary portfolios. Inside, you will find exact cost breakdowns, ownership categories, financing limits, the 2026 Golden Visa thresholds, and a precise step-by-step transaction timeline. Every figure is mapped to the 2026 property lifecycle, where sustained international capital inflows continue to compress ready-stock inventory. Explore our exclusive Dubai property listings to act before that inventory tightens further.

Key Takeaways

- Dubai property delivers tax-neutral returns. There is no annual property tax, no capital gains tax, and no inheritance levy on UAE real estate.

- Foreign ownership is decoupled from residency. Non-residents and expats hold full, permanent title in designated freehold zones without a visa.

- Gross rental yields range from 7.5% to 10%, outperforming capped western capitals like London and New York.

- The total acquisition cost runs roughly 6.5% above the base purchase price, driven by the 4% DLD registration fee and the 2% agency fee.

- The 2026 Golden Visa rules removed the upfront cash mandate. Only the total purchase value on the title deed needs to reach AED 2,000,000 to qualify for 10-year residency.

Why Invest in Dubai Real Estate?

Dubai leads global investment indices because it pairs structural tax neutrality with returns that western capitals cannot match.

The Sovereign Tax-Neutral Rule: Dubai real estate operates as a permanent structural safe haven for global wealth preservation. Total returns are entirely insulated from capital dilution by an absolute complete absence of annualized property taxes, capital gains taxes, stamp duties, or localized inheritance levies.

The market backs this with hard performance data. Dubai properties generate stable gross rental yields between 7.5% and 10% annually. Prime London assets typically return 2% to 4% gross, and Manhattan sits in a similar capped band meaning a Dubai title can produce double the rental income on equivalent capital deployment.

Investor protection is institutional, not informal. The Dubai Land Department (DLD) governs every title transfer, while the Real Estate Regulatory Agency (RERA) licenses brokers, audits escrow accounts, and enforces developer compliance. This regulatory architecture removes the counterparty ambiguity that deters cross-border buyers in less mature markets.

High-yield asset classes sit on both ends of the portfolio spectrum. Review our parent networks for Dubai Apartments for compressed-entry rental units and Dubai Villas for capital-appreciation-led freehold assets.

Who Can Purchase Property in the UAE?

Yes foreign nationals and expats can buy, sell, and lease property in Dubai with full legal ownership, and residency is not a prerequisite.

Property ownership in the UAE is completely decoupled from local residency mandates. You do not need a UAE visa, a local sponsor, or physical presence in the country to hold a freehold title. This is the single most common point of confusion among first-time border buyers, and the answer is unambiguous in the law.

The market recognizes four distinct buyer categories, all with the same ownership rights in freehold zones:

- Residents: Expats holding a valid UAE residency visa.

- Non-residents: Foreign nationals purchasing remotely from overseas.

- Expats: Foreign nationals living and working within the UAE.

- Foreign nationals: Overseas investors deploying foreign-sourced funds.

Non-resident purchases follow the same DLD transfer process as resident transactions, with documentation typically handled via power of attorney or secure remote signing. For complete legal clarity on cross-border ownership structures, see Can Expats Buy Property in Dubai, or browse our exclusive Dubai property listings to begin.

Freehold vs Leasehold: Understanding Ownership

Dubai offers two ownership models, and international portfolios focus almost exclusively on freehold for uncapped capital control.

The Title Permanence Principle: Freehold grants absolute ownership of both the physical property and the land beneath it, in perpetuity including the unconditional right to sell, lease, occupy, or transfer to heirs. Leasehold grants ownership of the unit only, for a fixed term, with the land retained by the freeholder.

Freehold is the standard for foreign capital. You hold the title indefinitely, capture 100% of any capital appreciation, and pass the asset to heirs without restriction. This is the structure that powers long-term wealth preservation.

Leasehold conveys use of the property for a fixed period, commonly up to 99 years, without ownership of the underlying land. At term expiry, rights revert to the freeholder. Leasehold appears predominantly in non-freehold areas and rarely suits investors seeking uncapped appreciation.

Designated freehold zones concentrate the city’s most liquid, highest-demand inventory. For the complete list of zones open to foreign ownership, see Freehold Property in Dubai.

The Step-by-Step Buying Process

A standard ready-property transaction in Dubai completes within 30 to 60 days, following a fixed six-stage sequence.

The process is fast because the DLD operates a centralized, digitized transfer system. Each step has a defined deliverable, moving from budget confirmation through Form F (the MOU) execution to developer clearance and final title registration.

How to Buy Property in Dubai: A Quick 6-Step Overview

- Define the budget and secure mortgage pre-approval. Confirm your total capital position and obtain a bank pre-approval letter if leveraging.

- Select the property type and freehold community. Match the asset class to your yield or appreciation objective.

- Engage a RERA-registered agent for verified due diligence. Authenticate developer credentials, escrow status, and clean title.

- Sign the Memorandum of Understanding (Form F) and pay the 10% deposit. This binds both parties under DLD-recognized terms.

- Obtain the No Objection Certificate (NOC) from the developer. Confirms zero outstanding service charges against the unit.

- Complete the DLD transfer and receive the Title Deed. Funds release, ownership registers, and the deed issues in your name.

For the exact document checklist and timeline mechanics at each clearance counter, see the Buying Property in Dubai Process.

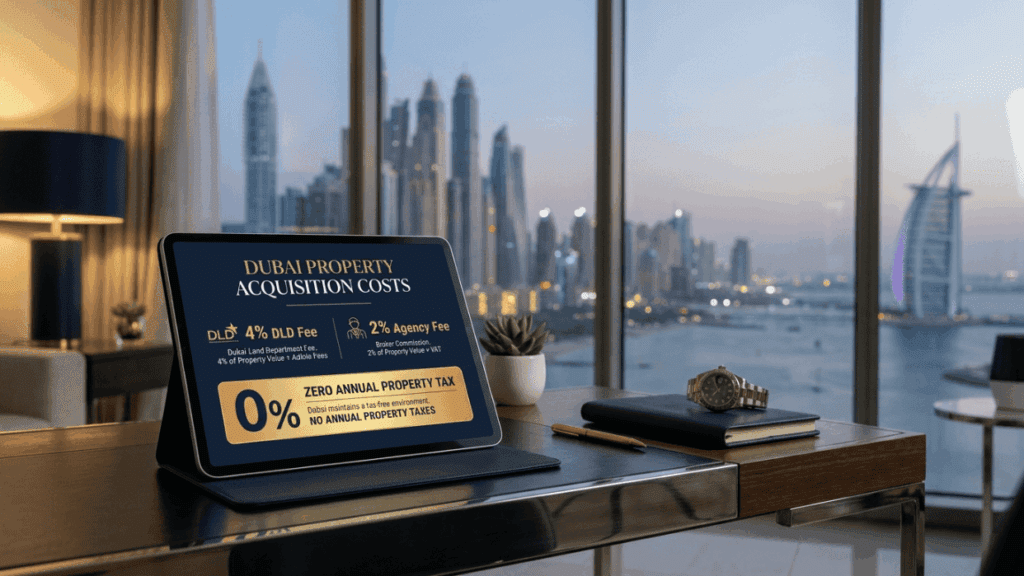

The Complete Cost of Ownership

The total upfront acquisition cost on a Dubai property runs approximately 6.5% above the base purchase price, with no recurring annual property tax thereafter.

Transparency on entry costs is non-negotiable for institutional planning. The table below itemizes every mandatory charge on a AED 1,000,000 ready property.

Table 1: Full Cost Breakdown of Buying a AED 1M Property in Dubai

| Expense Category | Percentage / Fixed Rate | Estimated Cost (AED) |

| Property Purchase Price | Base Value | 1,000,000 |

| DLD Registration Fee | 4% of Purchase Price | 40,000 |

| DLD Admin Fee | Fixed Fee | 580 |

| Real Estate Agency Fee | 2% of Purchase Price | 20,000 |

| Agency Fee VAT | 5% of Agency Fee | 1,000 |

| Property Registration Fee | Fixed (Properties > 500k) | 4,200 (incl. 5% VAT) |

| Total Estimated Acquisition Cost | ~6.5% Above Base Price | 1,065,780 |

The macro math is decisive. You pay roughly 6.5% in one-time transaction costs, then hold the asset with zero annual property tax for its entire lifecycle. In a market generating 7.5% to 10% gross yields, the entire upfront cost burden is typically recovered within the first year of rental income after which net yield protection compounds tax-free indefinitely.

Contact First Call Real Estate to speak with a Dubai property specialist today.

Off-Plan vs Ready Property

Off-plan suits cash-flow leverage maximizers; ready property suits cash-heavy investors demanding immediate ROI.

These are the two primary investment vehicles in the Dubai market, and the right choice depends entirely on your liquidity position and income timeline.

Table 2: Off-Plan vs Ready Property Comparison

| Feature | Off-Plan Property | Ready Property |

| Payment Structure | Flexible, linked to construction | Full payment upfront or via mortgage |

| Capital Appreciation | High potential before completion | Steady, driven by market trends |

| Rental Yield (ROI) | None until handover | Immediate income generation |

| Entry Price | Generally lower than market rate | Premium market value |

| Risk Profile | Mitigated by RERA escrow accounts | Minimal, tangible asset inspection |

Off-plan rewards investors who prioritize entry price and payment flexibility. Construction-linked installments protect cash flow, and the gap between launch price and handover value captures appreciation before you hold a finished asset. Ready property rewards cash-heavy buyers who want rental income from day one and the certainty of inspecting a tangible, completed unit.

⚠️ OQOOD REGISTRATION & ESCROW MANDATE: Regardless of whether you select a ready asset or an off-plan milestone plan, all financial allocations must be verified against official RERA-registered escrow records. For off-plan assets, confirm that an interim Oqood registration certificate is generated by the Dubai Land Department immediately upon execution of the Sales and Purchase Agreement (SPA) to secure your title before physical construction handovers.

Explore our current Dubai property listings at First Call Real Estate.

Financing Your Vision: Mortgage vs Cash

Cash delivers frictionless speed and maximum negotiation leverage; mortgages unlock leveraged returns within fixed 2026 LTV bands.

Cash acquisitions close fastest, eliminate interest exposure, and give buyers the strongest position at the negotiating table particularly on premium ready stock where vendors favor unconditional offers.

Mortgage financing extends reach through clearly capped loan-to-value (LTV) limits in 2026:

- Resident expats: Up to 80% LTV on ready inventory.

- Non-resident foreign nationals: A conservative 50% to 60% LTV bandwidth.

Leverage amplifies return on deployed capital, but interest rate exposure must be modeled across the holding period. To structure construction-linked payment schedules, review Buy Property on Installments in Dubai. To assess rate exposure and other liabilities before committing, review the Risks of Buying Property in Dubai.

Unlock the Dubai Golden Visa

A property investment of AED 2,000,000 secures a 10-year renewable UAE Golden Visa and as of February 2026, no upfront cash mandate applies to mortgaged assets.

The Residency Decoupling Principle: The Golden Visa grants 10-year renewable residency to the investor, their spouse, children, and domestic staff completely decoupled from employment status.

The 2026 update is the decisive shift for leveraged buyers. The historical requirement to pay a minimum of AED 1 Million (or 50% equity) upfront on mortgaged properties has been completely removed. To qualify, only the total purchase value stated on the DLD Title Deed or the Oqood off-plan contract needs to reach the AED 2,000,000 threshold, regardless of the outstanding mortgage debt balance, provided a bank No Objection Certificate (NOC) is submitted.

This means an investor can now leverage a AED 2,000,000 asset, carry a substantial mortgage, and still secure full 10-year residency for the family a structural efficiency unavailable before this year.

Partner with First Call Real Estate

Routing a Dubai transaction through a premier, RERA-licensed brokerage is the single most effective risk-mitigation decision a cross-border buyer can make.

First Call Real Estate delivers institutional-grade market insight, rigorous title and escrow due diligence, and direct access to the city’s most sought-after inventory. Every legal, financial, and strategic checkpoint from Form F execution to DLD title registration is managed by specialists who execute these transactions daily.

The advisory relationship does not end at handover. For complete asset lifecycle management, including disposition strategy, see How to Sell Property in Dubai.

Secure Your Position Before Inventory Tightens

Sustained international capital inflows are compressing ready-stock inventory through 2026, and the most liquid freehold assets are absorbing fastest. You now understand how to buy property in Dubai the ownership categories, the 6.5% cost structure, the 2026 financing bands, and the updated Golden Visa thresholds. Execution is what remains.

Contact First Call Real Estate today to secure your premier asset. Explore our exclusive Dubai property listings or schedule your strategic buyer consultation now.

Frequently Asked Questions

Can a foreigner buy property in Dubai?

Yes. Foreign nationals and expats can buy, sell, and lease property in Dubai with full legal ownership in designated freehold zones. UAE residency is not required to purchase or hold a title.

Do I pay taxes on property in Dubai?

No. Dubai imposes zero annual property tax, zero capital gains tax, and zero rental income tax. This structural tax neutrality makes it one of the most efficient real estate markets globally for wealth preservation.

How much do I need to invest to get a Golden Visa?

To qualify for the 10-year UAE Golden Visa, you must hold property with a total value of at least AED 2,000,000. As of February 2026, the upfront cash requirement on mortgaged properties has been removed, provided a bank No Objection Certificate is submitted.

What is the difference between freehold and leasehold?

Freehold provides complete, permanent ownership of both the physical property and the land it sits on. Leasehold offers ownership of the unit only for a fixed period, usually up to 99 years, predominantly in non-freehold areas.