Master the Exact Buying Property in Dubai Process

Securing Capital: Why the Exact Process Matters

UNPARALLELED MARKET. UNCOMPROMISING PRECISION.

Mastering the Buying Property in Dubai Process is the single most critical asset protection step you will take in the 2026 property cycle. This is not a casual acquisition exercise. It is a sequence of statutory milestones each one carrying defined legal liability and capital exposure that must be executed in exact order to secure a clean title deed and defend your earnest capital.

This roadmap exists for three distinct buyer profiles: cross-border cash buyers deploying liquid capital from abroad, overseas investors navigating the UAE legal system for the first time, and resident upgraders leveraging bank financing. Each faces the same regulatory architecture, supervised directly by the Dubai Land Department (DLD) the sovereign authority that registers and guarantees all property ownership in the emirate and the Real Estate Regulatory Agency (RERA), the regulatory arm governing broker conduct and contract standards.

The Statutory Capital Rule: In Dubai’s secondary and off-plan real estate markets, all financial milestones operate under fixed legal frameworks supervised directly by the DLD. A buyer must budget an upfront cash buffer of roughly 6.5% to 7% above the base purchase price to clear absolute sovereign transfer fees and agency percentages before a clean title deed is issued.

For a complete market orientation before you commit capital, review How to Buy Property in Dubai. The transaction framework below governs everything that follows.

Pre-Purchase Preparation: Audit and Approval

BUILD THE FOUNDATION. SECURE THE ASSET.

Serious buyers do not browse. They prepare. Before a single public portal is opened or a single viewing is scheduled, two technical actions must be completed: a liquid capital audit and a written mortgage pre-approval.

The Liquid Budget Audit. Calculate your total deployable capital against the full transaction cost not the headline purchase price. A complete audit accounts for the base property value, the fixed 4% DLD transfer fee, the registration trustee fee, the agency commission, and a contingency reserve for NOC and mortgage arrangement charges. Buyers who budget only the purchase price routinely encounter a settlement shortfall at the trustee office, triggering contract delay and deposit risk.

Mortgage Pre-Approval Criteria for 2026. Financing thresholds are fixed by Loan-to-Value (LTV) caps. Non-resident foreign nationals require a 50% down payment buffer on ready property the bank finances a maximum of 50% of the asset value. Resident expats qualify for up to an 80% LTV ready-property allowance, requiring a 20% down payment minimum (UAE Nationals secure marginally higher leverage). A written pre-approval is not a formality; it is the financing certainty that protects your deposit before any contract is signed.

RERA-Licensed Broker Verification. Every active agent in Dubai must hold a valid RERA broker card the official credential authenticating the agent’s license to transact and confirming the inventory presented is active and registered. Verify the card before engaging. Unlicensed intermediaries cannot lawfully process a DLD transfer.

For confirmation of foreign ownership eligibility and the legal structures available to overseas buyers, review Can Expats Buy Property.

The Exact Buying Property in Dubai Process

FROM SEARCH TO SIGNATURE. THE DEFINITIVE ROADMAP.

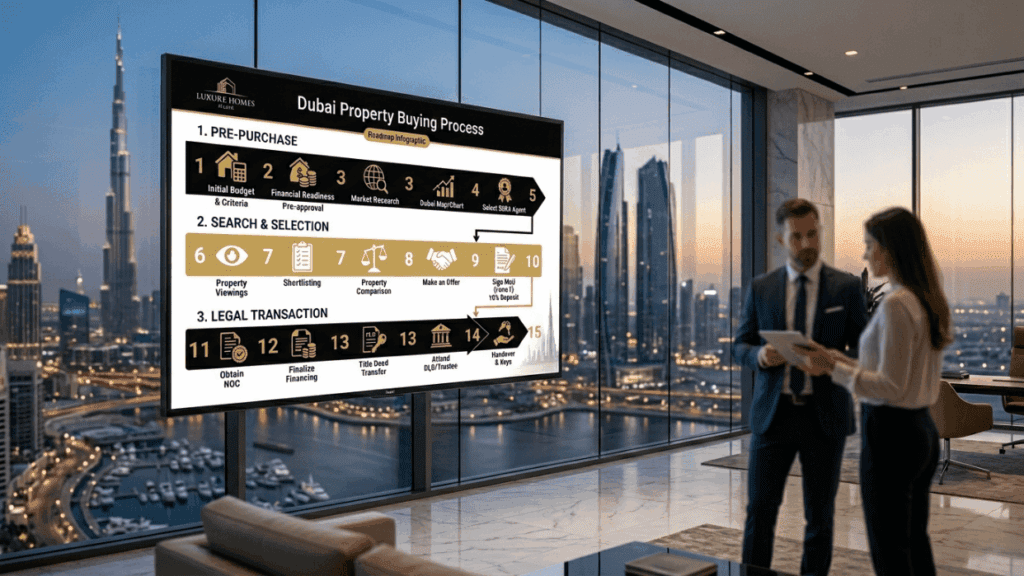

The complete transaction divides into fourteen sequential steps across three temporal blocks. Execute them in order. Each step carries a precise operational directive.

Pre-Purchase Steps

Step 1 — Audit liquid capital. Calculate total budget inclusive of all statutory costs, not the purchase price alone.

Step 2 — Secure mortgage pre-approval. If financing through a bank, obtain written pre-approval before viewing inventory.

Step 3 — Define acquisition criteria. Specify preferred property type, target area, and developer before engaging the market.

Search and Selection Steps

Step 4 — Engage First Call Real Estate. Access verified, active inventory through a RERA-licensed advisor.

Step 5 — Schedule site visits. Conduct physical or virtual inspections of shortlisted assets.

Step 6 — Compare shortlisted properties. Evaluate on price, size, view, and critically annual service charges.

Step 7 — Submit and negotiate the offer. Make a formal offer and negotiate the final price.

Legal Transaction Steps

Step 8 — Execute the contract. Sign Form F (MOU) for secondary market purchases, or the SPA for off-plan acquisitions.

Step 9 — Pay the deposit. Submit the earnest deposit, typically 10%, to secure the property.

Step 10 — Obtain the NOC. Secure the No Objection Certificate from the developer for secondary market transfers.

Step 11 — Settle DLD fees. Pay the 4% DLD transfer fee and the registration trustee fee.

Step 12 — Complete the transfer. Finalize ownership transfer at the DLD trustee office.

Step 13 — Receive the Title Deed. Obtain the definitive, registered proof of ownership.

Step 14 — Take possession. Receive keys and assume legal possession of the asset.

Legal Documents Explained: SPAs to Title Deeds

IRONCLAD AGREEMENTS. ABSOLUTE OWNERSHIP.

Five core legal instruments secure an investor’s title. Each performs a distinct function in the transaction chain.

Sales Purchase Agreement (SPA) — the definitive off-plan contract issued directly by the developer, binding the buyer to a structured installment schedule and the developer to defined construction and delivery obligations.

Form F (MOU) — the Memorandum of Understanding, the legally binding contract generated directly through the unified RERA system that outlines the definitive transactional boundaries between buyer and seller in the secondary market. Form F fixes the price, the deposit, and the transfer timeline.

No Objection Certificate (NOC) — the developer’s formal confirmation that all service charges on the unit are cleared and the developer holds no objection to the transfer. The NOC is mandatory for every secondary market resale and cannot be bypassed.

Oqood — the official DLD interim registration document recording off-plan ownership during the construction phase, before the final title deed is issued. Oqood registers your beneficial interest in the unit while the asset is under construction.

Title Deed — the ultimate proof of ownership issued by the DLD. A DLD-registered title deed is legally unchallengeable. Once your name is recorded on the deed, your ownership is sovereign-backed and absolute the definitive endpoint of the entire transaction.

For the geographic zones where foreign nationals secure full, perpetual ownership, review Freehold Property Dubai.

The True Cost of Buying: Exact Statutory Fees

TRANSPARENT COSTS. ZERO SURPRISES.

The 4% DLD transfer fee is fixed, mandatory, and non-negotiable. It cannot be waived, discounted, or absorbed by any party as a regulatory exemption. Every figure below is a statutory or market-standard cost the buyer must reconcile before the title deed is released.

| Cost Item | Amount | Paid By | When |

| DLD Transfer Fee | 4% of property value | Buyer | At transfer |

| Registration Trustee Fee | AED 4,200 (for AED 500K+) | Buyer | At transfer |

| Title Deed Issuance Fee | AED 580 | Buyer | At transfer |

| Agent Commission | 2% of property value | Buyer | At MOU signing |

| NOC Fee | AED 3,000–5,000 | Seller | Before transfer |

| Mortgage Arrangement Fee | 1% of loan (if applicable) | Buyer | At mortgage approval |

Off-Plan vs. Ready: The Buying Property in Dubai Process

CHOOSE YOUR PATH. MAXIMIZE YOUR ROI.

The Buying Property in Dubai Process diverges sharply between off-plan and ready assets in legal instrument, in payment structure, and in regulatory protection. Off-plan paths rely on registered escrow allocations and interim Oqood certificates, with capital released against construction milestones into a DLD-supervised escrow account. Ready assets focus on physical snag inspections and immediate title deed transfer, settled through full payment or a standard mortgage.

Off-plan financing for expats reaches a maximum 50% LTV, with the structured installment plan functioning as the primary leverage mechanism. The escrow account is the buyer’s core safeguard developer access to funds is conditional on verified construction progress.

| Process Step | Off-Plan | Ready Property |

| Legal Document | SPA | Form F (MOU) |

| Ownership Proof | Oqood certificate | Title Deed |

| NOC Required | No developer direct | Yes from master developer |

| DLD Registration | At SPA signing | At transfer |

| Payment Structure | Installment plan | Full payment or mortgage |

| Timeline | Construction period | 30 to 45 days |

| RERA Protection | Escrow account | DLD registration |

For staged-payment acquisition structures, review Buy Property on Installments. For the full off-plan procedural sequence, see Buying Process. Buyers targeting specific asset classes should consult Buy Apartment and Buy Townhouse for size-specific transaction guidance.

Timeline Guide: Executing the Dubai Property Transaction

RAPID EXECUTION. SEAMLESS TRANSITION.

Transaction velocity across the central Dubai corridor is high. Strict adherence to each phase duration is the only safeguard against contract breach and the subsequent forfeiture of your earnest deposit. The 2026 cycle operates on the following durations:

- Mortgage pre-approval: 5 to 10 business days.

- Property search and viewings: 1 to 4 weeks.

- MOU/SPA signing: 1 to 3 days post-offer.

- NOC issuance: 5 to 15 business days.

- DLD transfer: 1 to 3 business days after NOC clearance.

A standard cash secondary transaction wraps inside a clean 30-to-45-day window. The variable that most often extends this timeline is NOC processing build the developer’s 5-to-15-day window into your contract expiration date, not against it.

Speak to a First Call Real Estate transaction specialist to navigate your Dubai property purchase.

Common Process Mistakes to Avoid

PROTECT YOUR DEPOSIT. AVOID THE PITFALLS.

Mistakes in this process do not cost convenience. They cost deposits. The errors below are the most frequent points of capital forfeiture among first-time and cross-border buyers.

- Failing to budget the 4% DLD fee. Buyers who reconcile only the purchase price face a settlement shortfall at the trustee office. Budget the full 6.5% to 7% cash buffer in advance.

- Misaligning the contract timeline with expiration dates. A Form F carries a fixed transfer deadline. When the NOC or mortgage drawdown runs past that date, the buyer is in breach and the deposit is exposed.

- Ignoring service charge drag profiles. Annual service charges materially reduce net rental yield. A high-charge building can erase the ROI advantage of a lower purchase price.

- Transacting through unlicensed brokers. An agent without a valid RERA broker card cannot lawfully process a DLD transfer, exposing your earnest capital to an intermediary with no regulatory accountability.

- Signing an SPA without reading the clauses. Construction timelines, penalty provisions, and payment triggers are all defined in the contract. Review them before execution.

- Rushing without checking title deed history. Verify the seller’s registered ownership and confirm the unit carries no outstanding lien before committing the deposit.

⚠️ MORTGAGE PRE-APPROVAL CONTINGENCY ALERT: Never execute Form F (MOU) or submit a 10% earnest check prior to securing a written bank mortgage pre-approval. Under permanent RERA rules, if a buyer signs a purchase contract and subsequently fails to secure financing within the specified timeline, the seller holds the absolute legal right to retain the full 10% deposit as liquidation damages.

For the complete risk-mitigation framework governing high-value acquisitions, review Risks of Buying.

Secure Your Asset: Partner with First Call Real Estate

THE PINNACLE OF PROPERTY ACQUISITION. START TODAY.

Executing the exact Buying Property in Dubai Process is what separates a secure, sovereign-backed acquisition from a transaction exposed to breach and capital forfeiture. Every milestone from the liquid capital audit to the final DLD title deed operates under a fixed legal framework designed to protect the buyer who respects it.

First Call Real Estate is the definitive brokerage for secure, high-value property acquisitions in the UAE. Our RERA-licensed advisors manage the full transaction chain, authenticate active inventory, and execute each statutory milestone with absolute precision.

Explore the portfolio:

Explore Exclusive Property Listings

Execute with precision:

Book Your Transaction Consultation

Frequently Asked Questions

What is the process of buying property in Dubai?

The process follows fourteen sequential steps: budget audit, mortgage pre-approval, property selection, offer and negotiation, Form F (MOU) or SPA signing, 10% deposit, NOC issuance, DLD fee settlement, ownership transfer, and title deed issuance. A standard secondary transaction completes in 30 to 45 days under DLD and RERA supervision.

How long does it take to buy property in Dubai?

A cash secondary market transaction completes within 30 to 45 days. Mortgage pre-approval adds 5 to 10 business days, and developer NOC processing adds 5 to 15 business days. The final DLD transfer itself takes 1 to 3 business days.

What documents do I need to buy property in Dubai?

You require a valid passport (and Emirates ID for residents), a written mortgage pre-approval if financing, and a signed Form F (MOU) or SPA. The transaction concludes with the NOC, DLD fee receipts, and the issued title deed.

What are the fees involved in buying property in Dubai?

Buyers pay a fixed 4% DLD transfer fee, a registration trustee fee of AED 4,200 for properties above AED 500K, an AED 580 title deed issuance fee, and 2% agency commission. Mortgage buyers add a 1% loan arrangement fee. Budget a total cash buffer of 6.5% to 7% above the purchase price.

What is the difference between buying off-plan and ready property in Dubai?

Off-plan purchases use an SPA, register ownership via an Oqood certificate, and pay through installments protected by an escrow account. Ready properties use Form F (MOU), transfer via title deed, require a developer NOC, and settle through full payment or mortgage within 30 to 45 days.