How to Secure a Mortgage for Off Plan Property in Dubai 2026

Introduction: Contextualizing off-plan yields and introducing the Mortgage for Off Plan Property

Dubai real estate delivers rental yields between 6% and 10%. To hit those numbers, you need the right financing. Most global investors default to developer payment plans because they seem easy. This is a mistake.

After a decade arranging property finance at First Call Real Estate, I see the numbers clearly. A Mortgage for Off Plan Property costs less over time. It gives you better control of your cash flow and unlocks a clear path to the Golden Visa Dubai property 2026 requirements.

Property search starts with knowing your budget. Off Plan vs Ready Property to understand which asset class fits your strategy.

How UAE Mortgages Work for Off Plan

Buying off-plan means buying property before construction finishes. You do not hand your money directly to the developer. The Dubai Land Department (DLD) and the Real Estate Regulatory Agency (RERA) mandate the use of escrow accounts.

When you secure a Mortgage for Off Plan Property, your bank disburses funds directly to this escrow account. These payments are construction-linked. The developer only gets paid when they hit specific, verified building milestones.

This structure protects your capital. The bank acts as a secondary layer of due diligence against construction delays.

[Image: Construction cranes over the Dubai skyline showcasing off-plan developments]

Mortgage for Off Plan Property vs. Developer Payment Plans

Buyers constantly ask me to compare bank financing against developer plans. Here is the math. Developer plans require heavy, front-loaded payments. Bank mortgages spread the cost.

| Feature | Mortgage for Off Plan Property | Developer Payment Plan |

| Loan-to-Value (LTV) | Up to 50% for expats | Varies (often requires 40-60% during construction) |

| Interest/Profit Rates | Market rates (approx. 4% – 5.5%) | Often “0% interest” but priced into property premium |

| Tenure | Up to 25 years | Typically 2 to 5 years post-handover |

| DLD Registration | 4% + AED 4,200 admin fee | 4% (sometimes subsidized by developer) |

Check our guide on the Best Areas for Off Plan properties to see where these terms apply best.

Eligibility Requirements and Required Documents

Getting approved for an off plan mortgage Dubai requires specific documentation. The Central Bank of the UAE mandates strict debt-burden ratios.

You need a minimum monthly salary of AED 15,000 to qualify. Here is what you need to apply.

For UAE Residents:

- Passport, Emirates ID, and valid visa copy.

- Salary certificate addressed to the bank.

- Six months of original bank statements.

- Initial Sales and Purchase Agreement (SPA) from the developer.

For Non-Residents:

- Passport copy.

- Three to six months of bank statements from your home country.

- Proof of income (tax returns, payslips, or audited company financials).

- Copy of the developer’s SPA.

UAE Banks Offering Off Plan Property Mortgages in 2026

Not every bank finances off-plan projects. The ones that do rely on approved developer lists. You can choose a conventional mortgage or an Islamic mortgage UAE.

Islamic structures use Murabaha (cost-plus financing) or Ijara (lease-to-own). Both comply with Sharia law and offer competitive profit rates.

Here is how six major UAE banks compare for off-plan lending in 2026:

| Bank | Finance Type | Max Tenure | Min Salary |

| Emirates NBD | Conventional / Islamic | 25 Years | AED 15,000 |

| ADCB | Conventional / Islamic | 25 Years | AED 15,000 |

| Dubai Islamic Bank (DIB) | Islamic | 25 Years | AED 15,000 |

| Mashreq | Conventional / Islamic | 25 Years | AED 15,000 |

| First Abu Dhabi Bank (FAB) | Conventional / Islamic | 25 Years | AED 15,000 |

| Abu Dhabi Islamic Bank (ADIB) | Islamic | 25 Years | AED 15,000 |

LTV Ratios and Down Payments for Mortgage for Off Plan Property

The Central Bank of the UAE dictates exactly how much you can borrow. For off-plan properties in 2026, the rules are rigid.

If you are an expatriate or non-resident, the maximum Loan-to-Value (LTV) is 50%. You must cover the remaining 50% down payment from your own funds.

If you are a UAE National, the maximum LTV is 60%. This means a 40% down payment.

You must pay your portion to the developer first. The bank only steps in to fund the remaining 50% or 60% once your down payment clears the escrow account.

Step-by-Step Mortgage Application Process

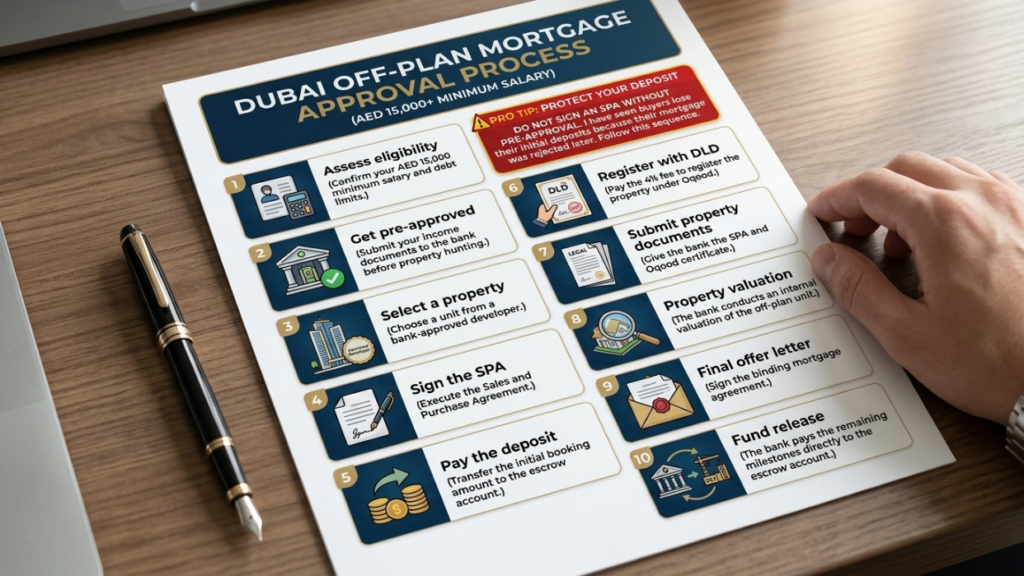

Do not sign an SPA without pre-approval. I have seen buyers lose their initial deposits because their mortgage was rejected later. Follow this sequence.

- Assess eligibility: Confirm your AED 15,000 minimum salary and debt limits.

- Get pre-approved: Submit your income documents to the bank before property hunting.

- Select a property: Choose a unit from a bank-approved developer.

- Sign the SPA: Execute the Sales and Purchase Agreement.

- Pay the deposit: Transfer the initial booking amount to the escrow account.

- Register with DLD: Pay the 4% fee to register the property under Oqood (initial register).

- Submit property documents: Give the bank the SPA and Oqood certificate.

- Property valuation: The bank conducts an internal valuation of the off-plan unit.

- Final offer letter: Sign the binding mortgage agreement.

- Fund release: The bank pays the remaining milestones directly to the escrow account.

Conclusion

A Mortgage for Off Plan Property limits your immediate capital outlay and maximizes your long-term rental yield. You get up to 25 years to pay off an asset that earns 6% to 10% annually.

UAE property finance 2026 offers high security through DLD regulations and escrow accounts. But you need to navigate strict LTV limits, bank-approved developer lists, and potential valuation gaps.

Secure your finance strategy before you sign an SPA. Contact the mortgage specialists at First Call Real Estate today to get your pre-approval started.

Investment Risks, Expert Tips, and FAQs

I’m gonna be straight with you. Off-plan investing carries risks.

Construction delays happen. If a project stalls, your money is tied up. Rely on RERA’s project tracking app to monitor actual site progress.

Valuation shortfalls are another reality. The bank finances the property based on their valuation, not the developer’s asking price. If you buy an apartment for AED 2 million, but the bank values it at AED 1.8 million, your 50% LTV is calculated on AED 1.8 million. You must pay the difference out of pocket.

FAQ: Can I sell my off-plan property before it is finished?

Yes. Most developers require you to pay 30% to 40% of the total price before they allow you to resell the SPA to a new buyer.FAQ: Does off-plan property qualify for the Golden Visa?

Yes. Under UAE property finance 2026 rules, buying an off-plan property worth at least AED 2 million makes you eligible for the Golden Visa, provided you meet the required equity threshold.